What is an Explanation of Benefits (EOB)? Complete Patient Guide to Reading and Using Your EOB

After every medical visit, your insurance company sends you a document called an Explanation of Benefits, commonly abbreviated as EOB. Most people glance at this document, assume it is just a routine notice, and set it aside without reading it carefully. This is a costly mistake. Your EOB is one of the most powerful tools available for protecting yourself from medical billing errors, insurance processing mistakes, and being overcharged for your healthcare. This complete guide teaches you everything you need to know about reading, understanding, and using your EOB effectively.

Disclaimer: This content is for educational purposes only and does not constitute legal or financial advice. Insurance plans vary significantly — always verify your specific benefits.

The Critical Difference Between an EOB and a Medical Bill

Understanding the difference between an EOB and an actual medical bill is the foundation of protecting yourself from overpaying. An Explanation of Benefits is a statement from your health insurance company explaining how they processed a claim submitted by your healthcare provider. It is not a bill. It does not mean you owe money — it is a record of insurance activity.

A medical bill, in contrast, is a request for payment from the healthcare provider showing what you owe after insurance has processed the claim. Many patients confuse their EOB for a bill and either pay amounts they do not owe or ignore actual bills thinking they are just EOBs. Always wait for an actual bill from the provider before making any payment, and always compare that bill to your EOB before paying anything. For help reading the actual bill side of this equation, see our guide on How to Read Your Medical Bill and Spot Errors.

When You Receive Your EOB

Insurance companies send EOBs after processing each claim submitted on your behalf. This typically happens within 2 to 4 weeks after your medical service. You may receive EOBs by mail, or you may access them online through your insurance company’s member portal. Many insurers allow you to set up email notifications when new EOBs are available, which is a useful feature for staying on top of your claims processing.

If you have a visit and never receive an EOB within 6 weeks, call your insurance company to inquire. The absence of an EOB may mean the claim was never submitted by the provider, which can lead to delayed billing problems later.

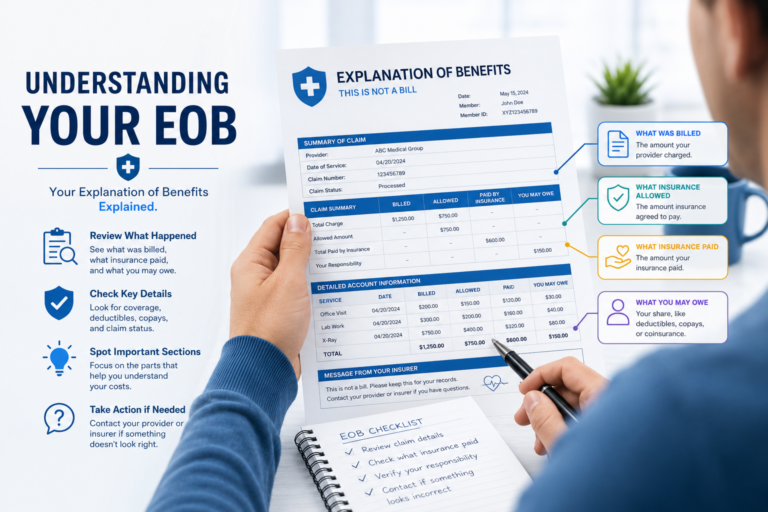

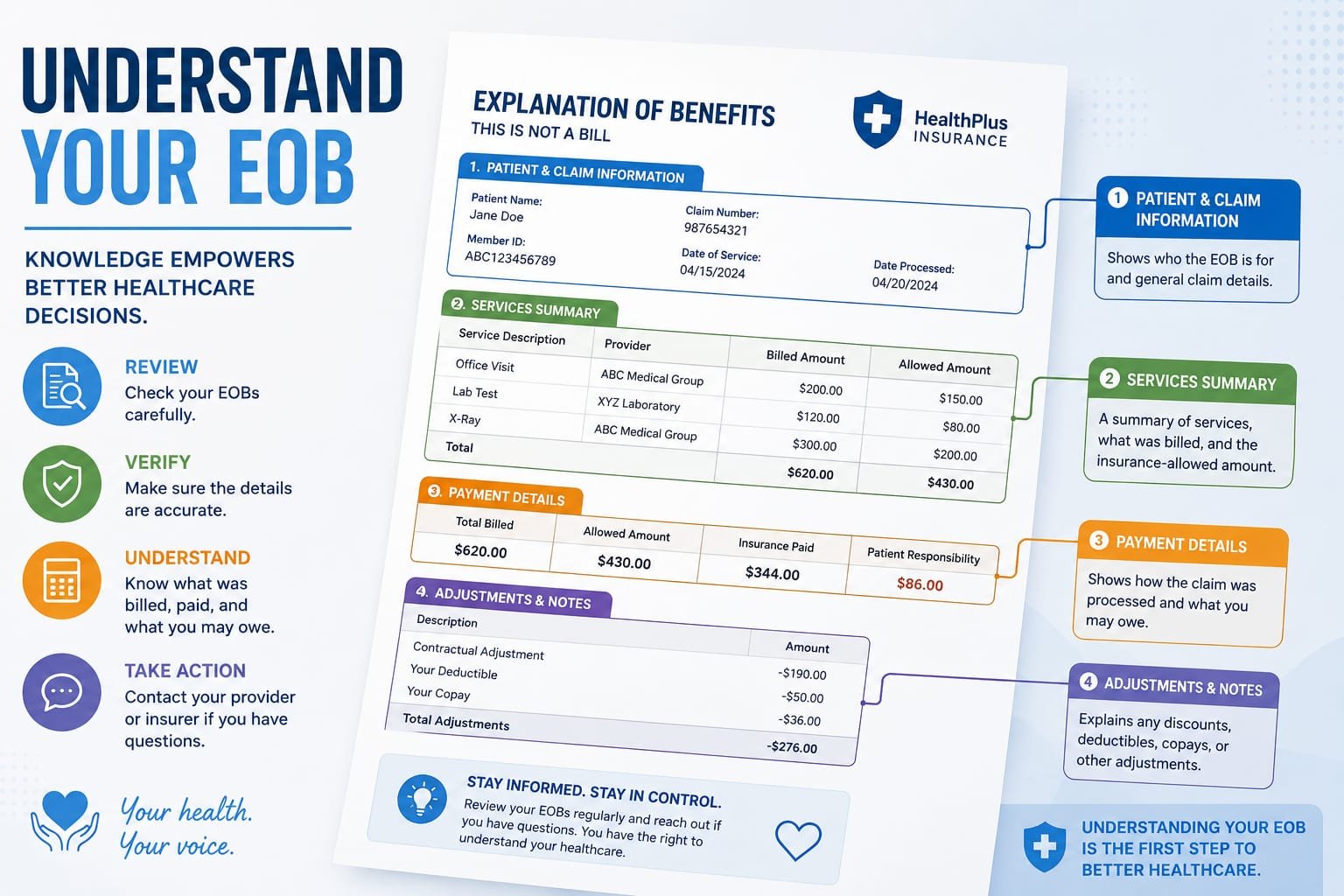

Anatomy of an EOB — Every Section Explained

Patient and member information: The top section of your EOB contains your name, member ID number, group number, and the patient’s name if different from the subscriber. Verify this information is correct on every EOB — errors in member information can cause significant claims processing problems.

Provider information: Lists the name and address of the healthcare provider who submitted the claim. Verify this matches the provider you actually saw. Occasionally claims are submitted by providers you did not visit, which can indicate billing errors or in rare cases fraudulent billing.

Dates of service: The dates on which services were provided. Verify these match your actual appointment dates. Incorrect dates can affect coverage determinations and cause unnecessary denials.

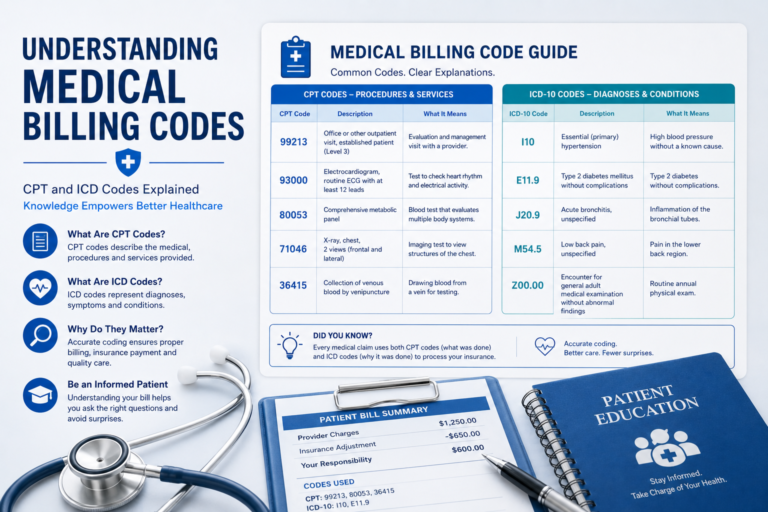

Service description and procedure codes: Each service is listed with a description and CPT code. This tells you exactly what was billed. Verify each service against your own memory of your visit. For help understanding billing codes, see our guide on Medical Billing Codes Explained for Patients.

Amount billed: What the provider charged before any insurance adjustments. This number is almost always higher than what anyone actually pays, because of negotiated rate agreements between providers and insurance companies.

Allowed amount (negotiated rate): The maximum amount your insurance company has contractually agreed to pay for each service with in-network providers. This is always lower than the billed amount and represents the true cost basis for your claim. The difference between the billed amount and the allowed amount is a plan discount you receive automatically by using in-network providers.

Plan paid: The actual dollar amount your insurance company paid to the provider. This is the allowed amount minus your deductible, copay, and coinsurance obligations.

Your responsibility: The amount you may owe after insurance payment. This includes any portion applied to your deductible, your copay, and your coinsurance percentage. This is the number to compare against your actual medical bill from the provider.

Deductible applied: How much of the claim was applied to your annual deductible. Tracking this helps you know how close you are to meeting your deductible, after which your insurance pays a higher percentage.

Out-of-pocket applied: How much of the claim counts toward your annual out-of-pocket maximum. Once you reach your out-of-pocket maximum, insurance typically covers 100 percent of covered services for the remainder of the year.

How to Compare Your EOB to Your Medical Bill

This is the most important action you can take to protect yourself from medical billing errors. When you receive both your EOB and a bill from your provider, place them side by side and compare them systematically.

First, verify the services listed on both documents match. The same CPT codes should appear on both. Second, verify the dates of service match. Third, check that the amount your provider is billing you matches the “your responsibility” section of your EOB. If your provider bills you more than your EOB shows as your responsibility, you may be being overcharged and should contact the provider’s billing department immediately.

Common mismatches include providers billing the full charged amount rather than the allowed amount, providers billing for denied services without first going through the appeal process, and mathematical errors in calculating patient responsibility. Each of these can cost you significant money if not caught and corrected.

EOB Red Flags That Require Immediate Action

Certain findings on your EOB require immediate follow-up action. Contact your insurance company right away if you see any of the following: services or procedures you do not recognize or did not receive, dates of service that do not match your actual appointments, a claim processed as out-of-network when you intentionally used an in-network provider, your deductible or out-of-pocket calculation appearing incorrect based on your plan documents, the same service appearing multiple times suggesting duplicate billing, or a claim that shows a different provider than who actually treated you.

Any of these red flags may indicate billing errors, insurance processing mistakes, or in rare cases fraudulent billing. Early detection is critical — these issues become much harder to resolve after payments have been made.

Understanding EOB Denial Codes

When your EOB shows a denied service, it will include a denial code and a brief explanation. Common denial codes include CO-4 for incorrect procedure code, CO-97 for benefit included in another service already adjudicated, CO-109 for claim not covered by this payer, and PR-1 for deductible amount. Each code points to a specific reason and a specific remedy.

Do not accept a denial without investigating it thoroughly. Many denials are the result of administrative errors that can be corrected simply by having the provider resubmit with the correct information. For denials that require a formal challenge, see our detailed guide on How to Appeal a Medical Bill Denial.

Organizing and Storing Your EOBs

Developing a system for organizing your EOBs prevents confusion and makes resolving problems much easier when they arise. Keep all EOBs for at least two years, and for major medical events such as surgeries, hospitalizations, or ongoing treatment for serious conditions, keep them indefinitely.

The most convenient approach for most people is accessing EOBs through the insurance company’s online member portal, where they are automatically stored and searchable. Download and save important EOBs as PDFs to your own secure storage as a backup. For paper-based organization, file EOBs chronologically within annual folders, with major medical events in their own clearly labeled folders.

Frequently Asked Questions About EOBs

Is an EOB the same as a bill? No. An EOB is an informational document from your insurance company showing how a claim was processed. A bill is a payment request from your healthcare provider.

What should I do if I disagree with my EOB? Contact your insurance company and ask for an explanation of any item you disagree with. If you believe the claim was processed incorrectly, ask for a review. If a service was denied that should be covered, file an appeal.

How long does it take to receive an EOB? Typically 2 to 4 weeks after your medical service, though this varies by insurer and how quickly the provider submits the claim.

Can I request an EOB for past claims? Yes. You can access historical EOBs through your insurance company’s member portal or by calling member services and requesting them.

Conclusion

Your Explanation of Benefits is a powerful tool that most patients underuse. Reading every EOB carefully, comparing it to your medical bills, understanding denial codes, and acting quickly on red flags protects you from a significant source of financial loss — medical billing errors and insurance processing mistakes. Combined with careful review of your actual medical bills as explained in our guide on How to Read Your Medical Bill and Spot Errors, and knowing how to negotiate from our guide on How to Negotiate Your Medical Bill Down, your EOB knowledge gives you comprehensive protection against overpaying for healthcare.