How to Appeal a Medical Bill Denial: Complete Step by Step Guide

Receiving a medical bill denial feels overwhelming — especially when you are already dealing with illness, recovery, and the stress of medical care. But here is what most patients do not know: a denial is not the end of the road. Studies consistently show that patients who appeal medical bill denials win a significant percentage of those appeals. The process requires knowledge, persistence, and the right approach. This complete guide walks you through every step of appealing a medical bill denial successfully.

Disclaimer: This content is for educational purposes only and does not constitute legal or financial advice. Always consult qualified professionals for advice specific to your situation.

Why Medical Bills Get Denied — Understanding the Root Cause

Before you can appeal a denial effectively, you need to understand why it happened. Insurance companies deny claims for a variety of reasons, and each reason requires a different appeal strategy. The most common denial reasons include services deemed not medically necessary by the insurance company’s clinical reviewers, procedures that required prior authorization but were performed without it, care provided by out-of-network providers when in-network care was available, incorrect billing codes submitted by the healthcare provider, missing or incorrect patient identification information, and services that fall outside your specific plan’s coverage terms.

The denial letter you receive must legally explain the specific reason for the denial and your right to appeal. Read this letter extremely carefully and keep it — it is the foundation of your entire appeal strategy. If the denial reason is unclear, call your insurance company and ask for a detailed explanation before proceeding. Understanding the exact reason transforms your approach from general to targeted and dramatically increases your chances of success.

Your Legal Rights as a Patient — Know Before You Appeal

The Affordable Care Act established powerful protections for patients facing insurance denials. Every health insurance plan must provide an internal appeals process, and the insurer must inform you clearly of your right to appeal. You have the right to appeal any denied claim, have your appeal reviewed by a different person than the one who made the original denial decision, receive a decision on urgent appeals within 72 hours, and request an external review by an independent organization if your internal appeal fails.

The external review right is particularly powerful and widely underused. If your insurance company denies your internal appeal, an independent organization reviews your case with no connection to the insurer. Their decision is binding — meaning if they rule in your favor, your insurance company must pay. Research shows that patients win approximately 40 percent of external reviews. This is a significant tool that many patients never use simply because they do not know it exists.

Also read our detailed guide on How to Read Your Medical Bill and Spot Errors because many denials are based on billing errors that can be corrected without a formal appeal.

Step 1 — Request the Complete Claim File Immediately

The most important first step is requesting your complete claim file from the insurance company. This file contains every document the insurer used to make the denial decision, including the clinical criteria applied, the guidelines referenced, and the specific reasons documented internally. You are legally entitled to this information at no charge.

Call the member services number on the back of your insurance card and specifically say: “I am appealing a claim denial and I am requesting my complete claim file including all documents used in the denial decision, the clinical criteria applied, and any utilization review guidelines referenced.” Request it in writing and keep records of when you called, who you spoke with, and what was promised. The claim file gives you invaluable insight into exactly what argument you need to make in your appeal.

Step 2 — Obtain a Detailed Letter of Medical Necessity From Your Doctor

A letter of medical necessity from your treating physician is the single most powerful document in any medical bill appeal. This is not a generic letter — it needs to be specifically tailored to address the insurance company’s stated reason for denial.

The letter should explain in clinical detail why the denied service was medically necessary for your specific condition and circumstances. It should reference relevant peer-reviewed medical literature and clinical guidelines supporting the treatment approach. It should explain specifically why alternative treatments suggested by the insurer were not appropriate for your situation. It should directly address the denial language used by the insurance company and refute it with medical evidence.

Contact your doctor’s office and ask specifically for a medical necessity letter addressing the denial. Provide them with a copy of the denial letter so they can address the specific denial reason. Most physicians and their staff are experienced with writing these letters — it is a routine part of patient advocacy in modern medical practice.

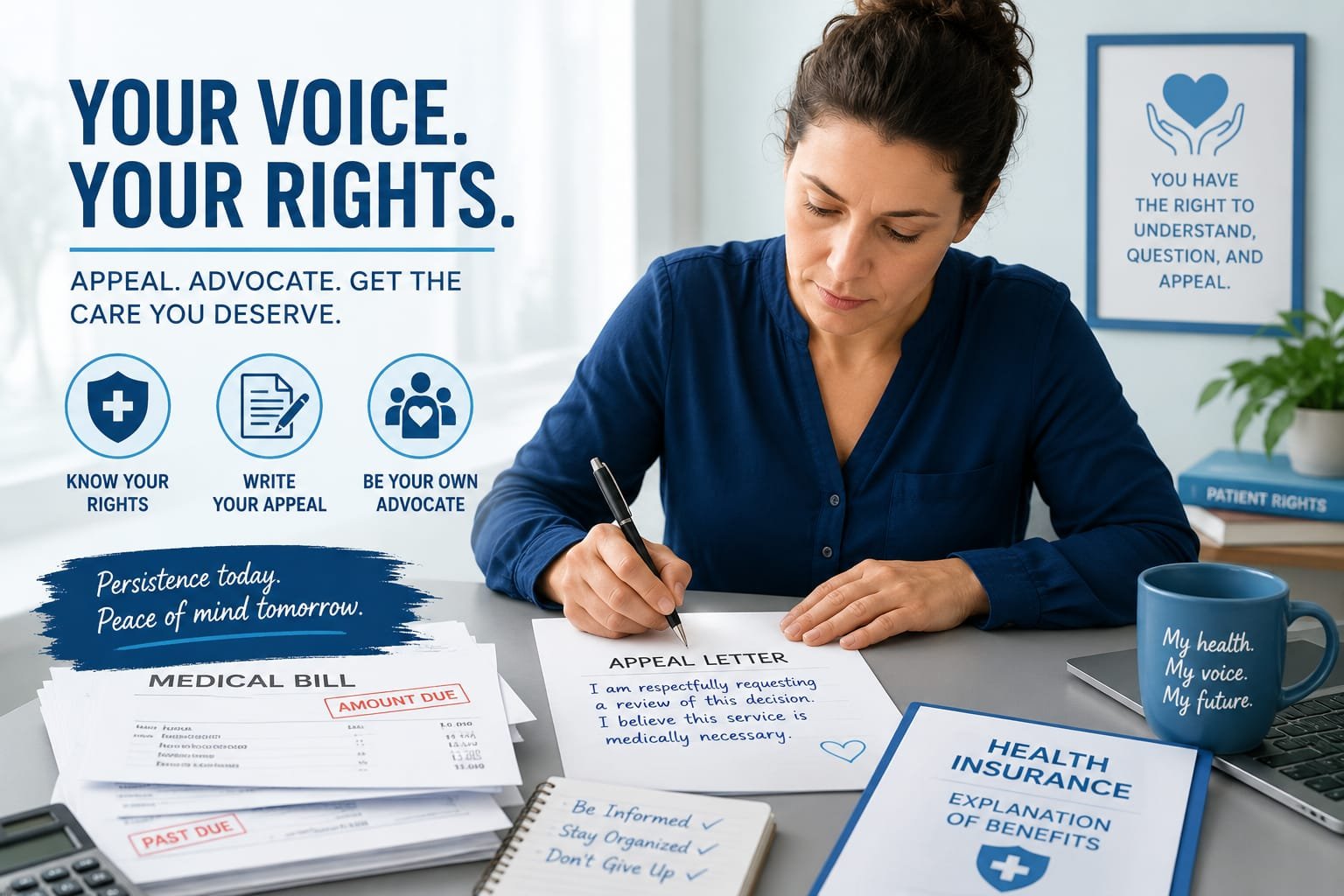

Step 3 — Write a Compelling Appeal Letter

Your appeal letter is your opportunity to make your case directly and professionally. The letter should be clear, factual, and focused entirely on why the denial was incorrect based on the specific denial reason cited.

Begin your letter with your full name, member ID number, date of birth, the claim number, date of service, and the name of the service or procedure being appealed. State clearly in the opening paragraph that you are formally appealing the denial of claim number [X] dated [date] and explain briefly why the denial was incorrect.

In the body of the letter, address the denial reason point by point. If the denial was based on medical necessity, reference your physician’s letter and any clinical guidelines supporting the treatment. If the denial was based on a coding error, explain the correct code and why it applies. If the denial was based on prior authorization issues, explain the circumstances and why the care was urgent or why prior authorization was not obtained.

Close the letter by listing all attached documentation, requesting a review by a different reviewer than the original denial, and providing your contact information for any questions. Keep the tone professional and factual throughout — emotional arguments are far less effective than clinical and administrative evidence.

Step 4 — Gather and Organize Supporting Documentation

A strong appeal is supported by thorough documentation. Gather and include your physician’s letter of medical necessity, relevant sections of your medical records supporting the need for the service, a copy of your insurance plan documents showing coverage for the service, published clinical guidelines or peer-reviewed research supporting the treatment, and the Explanation of Benefits showing how the claim was processed.

Organize everything clearly and include a cover page listing every document included in the appeal package. Number the pages and refer to specific page numbers when making arguments in your appeal letter. A well-organized, thoroughly documented appeal communicates seriousness and professionalism that disorganized submissions cannot.

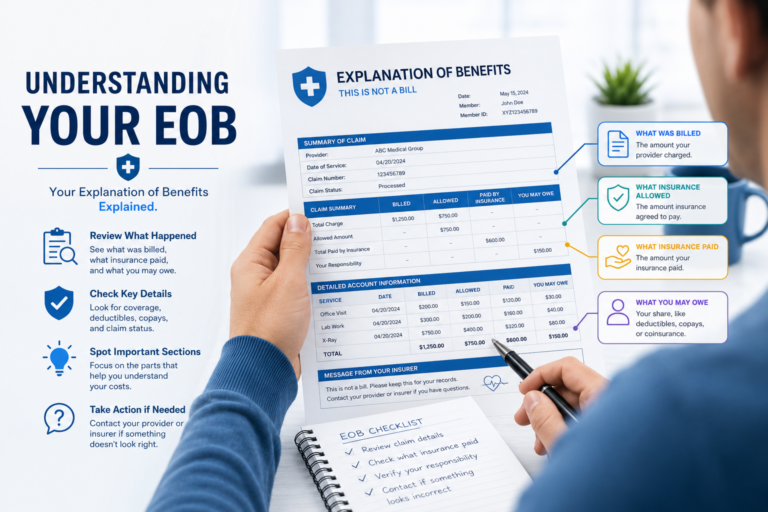

For understanding how to read your Explanation of Benefits and compare it to your medical bill, see our guide on What is an Explanation of Benefits.

Step 5 — Submit Before the Deadline and Track Everything

Appeals have strict deadlines that vary by plan and denial type — typically ranging from 30 to 180 days from the denial date. Missing the deadline forfeits your right to appeal, so act promptly. Submit your complete appeal package via certified mail with return receipt requested so you have documented proof of submission with a date stamp.

After submitting, follow up by phone within one week to confirm receipt and ask for a reference number and estimated timeline for the decision. Insurance companies are required to decide internal appeals within specific timeframes — typically 30 days for standard appeals and 72 hours for urgent appeals. Track every communication in a log including dates, names of representatives, and summaries of conversations.

Step 6 — Request External Review if Internal Appeal Fails

If the insurance company upholds the denial after your internal appeal, your journey is not over. Request an independent external review immediately. This right is guaranteed under federal law for most insurance plans. The external reviewer is completely independent of your insurance company and their decision is legally binding on the insurer.

To request external review, contact your insurance company and ask for external review instructions, or contact your state insurance commissioner’s office. The process typically involves submitting your documentation to the independent review organization, which then makes its decision based solely on medical evidence and your plan terms.

What to Do Even When Appeals Fail

Even unsuccessful appeals leave you with options. You can still negotiate the amount you owe directly with the provider or hospital. Our guide on How to Negotiate Your Medical Bill Down provides proven scripts and strategies for reducing your balance even after an insurance denial. Additionally, our guide on How to Get Free Help With Medical Bills covers charity care, patient advocacy organizations, and other resources that can help reduce or eliminate remaining balances.

Frequently Asked Questions About Medical Bill Appeals

How long does a medical bill appeal take? Internal appeals typically take 30 to 60 days for standard decisions. Urgent appeals must be decided within 72 hours. External reviews generally take 45 to 60 days.

Does appealing a medical bill hurt my credit? No. Filing an appeal does not affect your credit. However, if you receive a final bill and do not pay or arrange a payment plan while collection occurs, that can affect credit. During the appeal process, most providers will hold collection activity.

Can I appeal a medical bill denial without a lawyer? Yes. The appeals process is designed to be accessible to patients without legal representation. However, for very large denials or complex situations, consulting a patient advocate or healthcare attorney may be worthwhile.

What is the success rate for medical bill appeals? Success rates vary widely by denial type and how thoroughly the appeal is prepared. Well-documented appeals with strong medical necessity letters have significantly higher success rates than poorly documented ones. External reviews succeed approximately 40 percent of the time.

Conclusion

A medical bill denial is a challenge, not a verdict. With the right knowledge, proper documentation, and persistent follow-through, many denials can be successfully overturned. Start by understanding the denial reason, get a strong medical necessity letter from your physician, write a targeted appeal letter, submit thorough documentation before the deadline, and use the external review process if needed. The financial stakes make this effort entirely worthwhile — and the process is more accessible than most patients realize.

Continue building your medical billing knowledge with our guides on How to Read Your Medical Bill and Spot Errors, What is an Explanation of Benefits, and How to Negotiate Your Medical Bill Down.