How to Dispute a Medical Bill With Your Insurance Company — Complete 2026 Guide

You paid your insurance premiums faithfully every month. Then you had surgery or a medical procedure — and your insurance company either denied the claim, paid far less than expected or left you with a bill you cannot afford. This happens to millions of Americans every year. And most of them simply pay whatever their insurance company says they owe — without ever questioning it. Here is what the insurance industry does not advertise: insurance claim decisions are wrong far more often than you think — and you have the legal right to appeal every single one. According to the Kaiser Family Foundation, insurance companies deny approximately 17% of all in-network claims. Of the patients who appeal those denials, more than 40% have their original decision overturned. That means nearly half of all people who challenge an insurance denial win. This complete guide gives you everything you need to dispute a medical bill with your insurance company — from understanding your Explanation of Benefits to filing a formal internal appeal and taking your case to an external reviewer if needed.

Step 1 — Understand Your Explanation of Benefits (EOB)

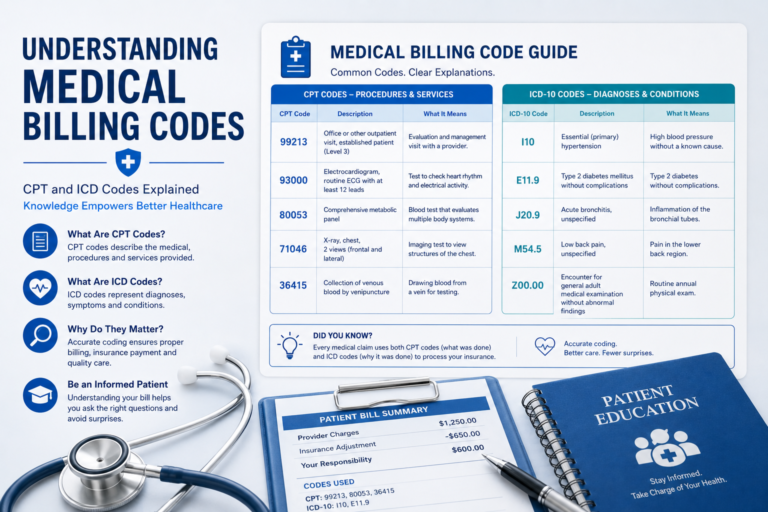

Before you can dispute anything, you need to understand what your insurance company actually did with your claim. An Explanation of Benefits (EOB) is a document your insurance company sends after processing a medical claim. It is not a bill — it is a statement showing: • What your provider charged • What your insurance company allowed (the negotiated rate) • What your insurance company paid • What you are responsible for paying • The reason for any denials or reductions

How to Read Your EOB

Every EOB contains these key sections: Service Description: What procedure or service was billed — listed by date and provider name. Amount Billed: The total amount your provider charged — usually the chargemaster rate. Allowed Amount: The negotiated rate your insurance company has agreed to pay for that service. This is typically much lower than the amount billed. Plan Paid: The amount your insurance company actually paid after applying your deductible, copay and coinsurance. Your Responsibility: The amount you owe after insurance payment. Reason Codes: These are critical. Every adjustment or denial includes a reason code — a short code that explains why the claim was reduced or denied. Look these up — they tell you exactly what to challenge.

Where to Find Your EOB

Your EOB should arrive by mail within 30 days of your claim being processed. Most insurance companies also make EOBs available through their online member portal. If you have not received your EOB, call the member services number on the back of your insurance card and request it.

Step 2 — Identify Why Your Claim Was Denied or Reduced

Before you can dispute effectively, you need to know exactly why your insurance company made the decision they did. Common reasons for claim denials include: Not medically necessary: The insurance company decided the procedure was not medically necessary — even if your doctor ordered it. This is the most common denial reason and one of the most successfully overturned on appeal. Out-of-network provider: The doctor or facility was not in your insurance network. This can often be disputed if you had no reasonable access to an in-network provider, especially in emergency situations. Prior authorisation not obtained: Some procedures require pre-approval from your insurance company. If your provider did not get this approval, the claim may be denied — but you can often appeal by showing medical necessity. Incorrect billing code: The provider used the wrong CPT or ICD code, causing the claim to be rejected. This is a billing error — not a genuine denial — and is relatively straightforward to correct. Coverage exclusion: The service is specifically excluded from your plan. Review your plan documents carefully — sometimes services are excluded only under certain circumstances. Coordination of benefits issue: If you have more than one insurance plan, there may be confusion about which pays first. This is an administrative issue that can usually be resolved quickly. Duplicate claim: The claim was submitted more than once. Again, this is an administrative error rather than a genuine denial. Timely filing limit exceeded: The claim was submitted after the deadline. Your provider is responsible for timely filing — if they missed the deadline, dispute this with both your provider and insurance company.

6

Step 3 — Gather Your Evidence Before Appealing

A successful insurance appeal is built on evidence. Before you write a single word of your appeal letter, gather these documents:

Documents to Collect

Your insurance policy documents: The Summary of Benefits and Coverage (SBC) and your full policy document. You are looking for the specific language that covers — or excludes — the service in question. Your doctor’s medical records: The clinical notes, test results, referral letters and any documentation showing why the procedure was medically necessary. A letter of medical necessity from your doctor: This is one of the most powerful documents in any appeal. Ask your doctor to write a detailed letter explaining why the specific procedure was medically necessary for your condition. Include clinical guidelines, published research and professional standards that support their decision. The denial letter from your insurance company: This contains the specific reason code and the legal basis for the denial — which you will address point by point in your appeal. The EOB for the denied claim: Shows exactly what was submitted and what was denied. Clinical guidelines supporting the procedure: Look up guidelines from organisations like the American Medical Association (AMA), American College of Physicians or relevant specialty organisations that support the medical necessity of your procedure.

One Critical Step — Check Your Plan Documents

Read your Summary of Benefits and Coverage carefully. Look for: • The specific coverage language for the procedure in question • Any exceptions to coverage exclusions • The appeals process and deadlines — these vary by plan • Whether your plan is fully-insured (state regulated) or self-funded (federally regulated under ERISA) This distinction matters because it affects which external review process applies to you if your internal appeal fails.

Step 4 — File Your Internal Appeal

Every insurance company is required by law to have an internal appeals process. Under the Affordable Care Act (ACA), you have the right to appeal any denied or reduced claim through this process.

Deadlines — Do Not Miss These

• Urgent care appeals: Insurance company must respond within 72 hours • Pre-service appeals: Insurance company must respond within 30 days • Post-service appeals: Insurance company must respond within 60 days • Your filing deadline: Most plans require you to file within 180 days of the denial — check your plan documents for the exact timeframe

How to File Your Internal Appeal

Step 1: Call the member services number on your insurance card. Ask for: • The exact name and address of the appeals department • The specific process for submitting an appeal for your type of denial • Confirmation of the deadline for your appeal Step 2: Write your appeal letter (template below) Step 3: Assemble all supporting documents Step 4: Submit by certified mail with return receipt — this creates a paper trail proving your appeal was received on time Step 5: Follow up in writing after 14 days if you have not received confirmation

Appeal Letter Template — Copy and Personalise

“[Your Name] [Your Address] [Your Insurance ID Number] [Date] [Insurance Company Name] Appeals Department [Insurance Company Address] Re: Appeal of Claim Denial Claim Number: [Claim Number] Date of Service: [Date] Provider: [Provider Name] Service Denied: [Description of Service] Dear Appeals Department, I am writing to formally appeal the denial of the above-referenced claim, which I received on [date of denial letter]. Your denial states that [quote the specific reason for denial from the denial letter]. I respectfully disagree with this determination for the following reasons: [Reason 1 — Address the specific denial reason with evidence] [Reason 2 — Reference medical necessity documentation] [Reason 3 — Cite relevant plan language that supports coverage] Enclosed with this letter please find the following supporting documentation: • Letter of medical necessity from [Doctor’s Name, MD] • Relevant sections of my policy documents • Clinical guidelines supporting medical necessity • My complete medical records related to this service I request that you overturn your denial and process this claim for payment in accordance with my plan benefits. If you uphold the denial, I request a full written explanation of the clinical and policy basis for your decision, including the specific plan language relied upon and the specific clinical criteria applied. Please confirm receipt of this appeal and advise me of the timeline for your decision. Sincerely, [Your Name] [Your Phone Number] [Your Email Address]”

Step 5 — Request an External Review if Your Appeal is Denied

If your insurance company upholds its denial after your internal appeal, you have one more powerful option: external review. External review is a process where an independent organisation — not connected to your insurance company — reviews your case and makes a binding decision. Under the ACA, insurance companies are legally required to accept the decision of an external reviewer.

Who Handles External Reviews?

For fully-insured plans (most individual and small employer plans): Your state Insurance Commissioner oversees the external review process. Contact your state insurance department to file a request. For self-funded employer plans (most large employer plans): The federal external review process applies. Contact the US Department of Labor Employee Benefits Security Administration (EBSA) at dol.gov/agencies/ebsa.

How to Request External Review

Step 1: Request external review within 4 months of your internal appeal denial (deadlines vary — check your denial letter) Step 2: Complete the external review request form from your state insurance department or the federal EBSA Step 3: Submit the same supporting documentation you used for your internal appeal Step 4: An independent medical reviewer will examine your case Step 5: The reviewer issues a decision within 45 days (or 72 hours for urgent cases) Step 6: If the reviewer overturns the denial — your insurance company is legally required to pay the claim The external review process costs nothing and has a strong track record. According to data from the Government Accountability Office (GAO), patients win external review cases approximately 39% to 59% of the time depending on the type of claim.

Step 6 — Dispute Billing Errors With Your Insurance Company

Sometimes the problem is not a genuine denial — it is a billing error that caused the claim to be processed incorrectly. These are actually easier to resolve. Common insurance billing errors include: • Wrong member ID number on the claim — causes automatic rejection • Incorrect date of service — claim does not match medical records • Wrong provider NPI number — claim attributed to wrong doctor • Coordination of benefits error — wrong insurance billed first • Incorrect diagnosis code — ICD code does not support the procedure billed

How to Dispute a Billing Error With Insurance

Call member services and say: “Hello, I am calling about a claim that I believe was denied due to a billing error rather than a coverage issue. My claim number is [X] for services on [date]. The denial reason indicates [reason] but I believe this is incorrect because [explain the error]. Could you please reprocess this claim with corrected information?” In most cases, billing errors can be corrected and the claim reprocessed without going through the formal appeals process.

Phone Scripts for Insurance Disputes

Opening Call — Understanding Your Denial

“Hello, my name is [name] and my member ID is [ID]. I received a denial for claim number [X] dated [date]. I would like to understand exactly why this claim was denied and what my options are for appealing this decision. Could you please walk me through the specific reason for the denial and give me the exact steps and deadlines for filing an appeal?”

Requesting a Peer-to-Peer Review

A peer-to-peer review is where your doctor speaks directly with the insurance company’s medical director. This is one of the most effective tools for overturning medical necessity denials. Ask your doctor’s office to call the insurance company and request this: “This is Dr [Name]’s office calling about a medical necessity denial for patient [name], claim number [X]. We would like to request a peer-to-peer review with your medical director. When is the earliest available time for this review?” Studies show that peer-to-peer reviews overturn medical necessity denials in 60% to 75% of cases. Always request this before filing a formal appeal.

Escalation Script — When You Are Getting Nowhere

“I understand you cannot resolve this directly. I would like to speak with your supervisor or a senior appeals specialist. I have been trying to resolve claim number [X] since [date] and I need someone with the authority to review this case comprehensively. This is now affecting my ability to receive necessary medical care.”

Real Case Study — How One Patient Won a $28,000 Denial

When Patricia M. from Ohio underwent emergency gallbladder surgery, her insurance company denied $28,000 of the claim — stating that the surgery was “not medically necessary” because she had not tried non-surgical treatment first. Patricia followed every step in this guide. Here is what happened: Step 1 — Requested peer-to-peer review: Her surgeon called the insurance company’s medical director directly and explained that emergency gallbladder removal is the accepted standard of care for acute cholecystitis — non-surgical treatment was not an appropriate option given the severity of her condition. Result: The medical director agreed to reconsider but still upheld the denial. Step 2 — Filed internal appeal: Patricia submitted a detailed appeal letter with her surgeon’s letter of medical necessity, the American College of Surgeons clinical guidelines supporting emergency surgery, her emergency room records and her discharge summary. Result: The internal appeal was denied again — but the insurance company’s reasoning was now clearly documented. Step 3 — Requested external review: Patricia filed for external review through Ohio’s Department of Insurance. An independent physician reviewed her case within 30 days. Result: The external reviewer overturned the denial completely, finding that emergency gallbladder surgery met all criteria for medical necessity. Final outcome: Insurance company paid $28,000. Patricia paid only her standard deductible. “I almost gave up after the first denial,” Patricia said. “I had no idea I had the right to external review. That changed everything.”

Special Situations — What to Do When

When Your Out-of-Network Bill Is Covered by the No Surprises Act

The No Surprises Act, which took effect January 2022, protects you from unexpected out-of-network bills in specific situations: • Emergency care at any facility — regardless of network status • Non-emergency care at an in-network facility where you see an out-of-network provider without being informed • Air ambulance services from out-of-network providers Under this law, if your situation qualifies, you can only be charged your in-network cost-sharing amount — no matter what the out-of-network provider charges. If you receive an unexpected out-of-network bill that should be covered by the No Surprises Act: 1. File a complaint at cms.gov/nosurprises 2. Call the No Surprises Help Desk: 1-800-985-3059 3. Contact your state Insurance Commissioner

When Your Insurance Company Takes Too Long

Insurance companies are legally required to respond to appeals within specific timeframes. If they miss these deadlines: • Document every contact — dates, names, what was said • Send a formal written complaint to your state Insurance Commissioner • Contact your employer’s HR department if you have employer-sponsored insurance — employers have leverage with insurance companies that individuals do not

When You Cannot Afford to Pay While Appealing

While your appeal is pending: • Send the provider a written notice that the claim is under appeal with your insurance company • Request that the provider place your account on hold pending resolution • Most providers will agree to this — they would rather wait for insurance payment than send you to collections

When to Get Professional Help

Consider hiring a patient advocate or healthcare attorney if: • The denied amount exceeds $5,000 • You have exhausted internal and external appeals unsuccessfully • The denial involves a life-sustaining treatment or urgent ongoing care • You believe bad faith insurance practices are involved The Patient Advocate Foundation (patientadvocate.org) offers free case management services for patients dealing with insurance denials related to serious illness.

Tracking Your Dispute — Keep a Detailed Log

Create a simple log for every insurance dispute: | Date | Contact | Action Taken | Response | Next Step | |——|———|————-|———-|———–| Record every phone call, every letter sent, every response received. This documentation is essential if your case escalates to external review, a state complaint or legal action. Save copies of every document sent and received — including screenshots of online submissions.

Frequently Asked Questions

How long does the insurance appeal process take?

Internal appeals for post-service claims must be decided within 60 days. Urgent care appeals must be decided within 72 hours. Pre-service appeals must be decided within 30 days. External reviews are typically completed within 45 days, or 72 hours for urgent cases. The entire process from initial denial to external review decision can take 3 to 6 months for non-urgent cases.

Can I continue receiving treatment while my appeal is pending?

Yes — but you need to be careful. If you have a continuing course of treatment that was approved and your insurance company tries to reduce or terminate that treatment, you have the right to continue treatment at no additional cost while the appeal is pending. This is called the “continuity of care” protection under the ACA.

What is a peer-to-peer review and should I request one?

A peer-to-peer review is a direct conversation between your treating physician and the insurance company’s medical director. It is one of the most effective tools for overturning medical necessity denials — success rates range from 60% to 75%. Always request this before filing a formal appeal. Ask your doctor’s office to call the insurance company to arrange it.

What if my employer’s insurance plan denies my appeal?

Large employer plans (self-funded plans) are governed by federal law (ERISA) rather than state insurance law. For these plans, the external review process is handled federally through the Department of Labor. Contact the Employee Benefits Security Administration (EBSA) at 1-866-444-3272 or dol.gov/agencies/ebsa.

Can I appeal a denial from Medicare or Medicaid?

Yes. Medicare and Medicaid have their own specific appeals processes. For Medicare, you have 5 levels of appeal starting with redetermination by the Medicare contractor. For Medicaid, contact your state Medicaid agency. The basic principles in this guide apply but the specific processes differ from private insurance.

What if my doctor says the procedure is necessary but insurance still denies it?

Request a peer-to-peer review immediately. Then file an internal appeal with your doctor’s letter of medical necessity, clinical guidelines from relevant medical associations, your medical records and any published research supporting the procedure. If the internal appeal fails, proceed to external review — independent reviewers frequently overturn denials when strong clinical evidence is provided.

Is there a cost to file an insurance appeal?

Internal appeals are free — insurance companies cannot charge you to appeal a decision. External reviews typically cost $25 or less, and this fee is waived if the review overturns the denial. In most states, external review is completely free.

Your Insurance Dispute Action Plan

Do not accept an insurance denial as final. Here is your complete action plan: 1. Get your EOB — understand exactly what was denied and why 2. Request a peer-to-peer review — ask your doctor’s office to call the insurance medical director 3. Gather all evidence — medical records, medical necessity letter, clinical guidelines, policy documents 4. File your internal appeal — use the template in this guide, send by certified mail 5. Request external review — if internal appeal fails, file immediately with your state or federal reviewer 6. File a complaint — contact your state Insurance Commissioner if the insurance company is non-responsive or acting in bad faith 7. Get professional help — contact the Patient Advocate Foundation for free case management if the amount is significant Remember: nearly half of all insurance appeal cases that go to external review are overturned in the patient’s favour. The system is designed to be difficult — but it is not unbeatable. For your next step — once your insurance dispute is resolved — read our complete guide: How to Negotiate Medical Bills After Surgery — Save Up to 80% for the full negotiation strategy to use with your hospital directly. And if you need help finding billing errors before disputing with insurance, see our guide: How to Request an Itemised Medical Bill — Free Script Inside.Medical and Financial Disclaimer: The information on FightMedicalBill.com is for educational purposes only and does not constitute medical, legal or financial advice. Always consult a qualified professional for advice specific to your situation. Insurance laws and regulations vary by state and plan type and change regularly. Always check your specific plan documents for the rules that apply to you.