What to Do If You Can’t Pay a Hospital Bill — 6 Options Most People Don’t Know About

You just received a hospital bill that you have absolutely no idea how to pay. Maybe it is $5,000. Maybe it is $50,000. Either way, it feels impossible — and the fear of what happens next can be paralysing. Here is what most people do in this situation: they ignore the bill and hope it goes away. Or they panic and make the minimum payment on a credit card, racking up interest on an already unmanageable debt. Here is what you should do instead: take a breath and read this guide. There are at least 6 options available to patients who cannot pay their hospital bills — and most people have never heard of most of them. Hospitals do not advertise these options because it is not in their financial interest to do so. But they exist. And you have a right to access them. This guide walks you through every option available to you — from charity care and financial hardship programs to payment plans, debt negotiation and legal protections. By the end, you will have a clear action plan regardless of your income level or financial situation.

The Most Important Thing to Do First — Do NOT Ignore the Bill

Before we get into your options, there is one rule you must follow: Never ignore a hospital bill — even if you cannot pay it. Ignoring a hospital bill does not make it go away. It starts a clock running toward a series of consequences that get progressively worse: • After 30–60 days: late fees and interest may begin • After 90–120 days: the hospital may send your account to a collections agency • After collections: your credit score can be significantly damaged • After 180+ days: the hospital or collections agency may file a lawsuit • After a judgement: wage garnishment or bank account levy becomes possible The moment you engage with the hospital — even just to say “I cannot pay right now but I want to work something out” — the clock slows dramatically. Most hospitals will not send an account to collections while you are actively communicating and working toward a resolution. Contact the billing department as soon as possible. Even a single phone call changes your situation significantly.

Option 1 — Apply for Charity Care (Can Eliminate 50–100% of Your Bill)

This is the option most patients never know exists — and it is the most powerful tool available to people who genuinely cannot afford their hospital bill. What is charity care? Charity care is a financial assistance program that every non-profit hospital in the United States is legally required to offer. Under the Internal Revenue Service (IRS) rules governing tax-exempt organisations, non-profit hospitals must provide free or discounted care to patients who cannot afford to pay — as a condition of maintaining their tax-exempt status. This is not optional for non-profit hospitals. It is the law. And the majority of hospitals in the United States — approximately 60% — are non-profit organisations.

Who Qualifies for Charity Care?

Eligibility is based primarily on your income relative to the Federal Poverty Level (FPL). Thresholds vary by hospital but typical guidelines are: • Under 200% of FPL — most hospitals offer 100% free care (complete bill forgiveness) • 200–300% of FPL — typically 75–80% reduction • 300–400% of FPL — typically 50% reduction • Over 400% of FPL — sliding scale discounts, still worth applying For 2026, 200% of the Federal Poverty Level is approximately: • $30,120 for a single person • $40,880 for a family of 2 • $51,640 for a family of 3 • $62,400 for a family of 4 If your household income falls below these thresholds, you have an excellent chance of qualifying for significant — or complete — bill forgiveness.

How to Apply for Charity Care

Step 1: Call the hospital billing department and say: “Hello, I received a bill I am genuinely unable to pay. I would like to apply for your financial assistance or charity care program. Could you please tell me how to apply and what documents I need to provide?” Step 2: Request the financial assistance application form — hospitals are required to make this available. Step 3: Gather your documentation: • Recent pay stubs (last 2–3 months) • Most recent federal tax return • Bank statements (last 2–3 months) • Proof of expenses — rent, utilities, childcare • Any other income documentation Step 4: Complete and submit the application with all supporting documents. Step 5: Follow up within 10 business days if you have not received a response.

Important Tips for Charity Care Applications

• Apply even if you think you will not qualify. Many hospitals have more generous thresholds than their published guidelines suggest. • Apply retroactively. Most hospitals allow charity care applications for bills already incurred — sometimes going back 12 months or more. • Ask about self-pay discounts if you do not qualify for charity care — many hospitals offer 20–40% discounts for uninsured patients paying out of pocket. • Do not be embarrassed. This program exists specifically for situations like yours. Hospital financial counsellors process these applications every single day.

Option 2 — Request a Zero-Interest Payment Plan

If your income is too high to qualify for charity care but you still cannot pay the full bill at once, a payment plan is your next best option. Most hospitals offer payment plans — and many offer them at zero interest. This means you pay the same total amount, just spread over time, without any additional charges.

How to Request a Payment Plan

Call the billing department and say: “I would like to set up a payment plan for my outstanding balance. I want to confirm upfront that the plan will carry zero interest. What is the minimum monthly payment your hospital accepts?” Most hospitals accept minimum payments of $25 to $100 per month regardless of the total balance. Some hospitals have official policies accepting as little as $10 per month for patients demonstrating financial hardship.

Key Rules for Payment Plans

• Always get the agreement in writing before making your first payment — verbal agreements are not enforceable • Confirm zero interest in writing — some hospitals add interest after an initial promotional period • Make every payment on time — missing payments can void your agreement and trigger collections • Keep records of every payment — date, amount and payment method • Request a receipt or payment confirmation for every transaction

What If They Demand More Than You Can Afford?

If the hospital demands a monthly payment you genuinely cannot afford, say: “I understand your standard payment plan requirements. However, I can only afford [amount] per month right now given my current financial situation. I am committed to paying this debt — I just need the monthly amount to reflect what I can realistically manage. Can we work with [amount] per month?” Most billing departments have discretion to work with patients on payment amounts. If the front-line representative cannot help, ask to speak with a financial counsellor or billing supervisor.

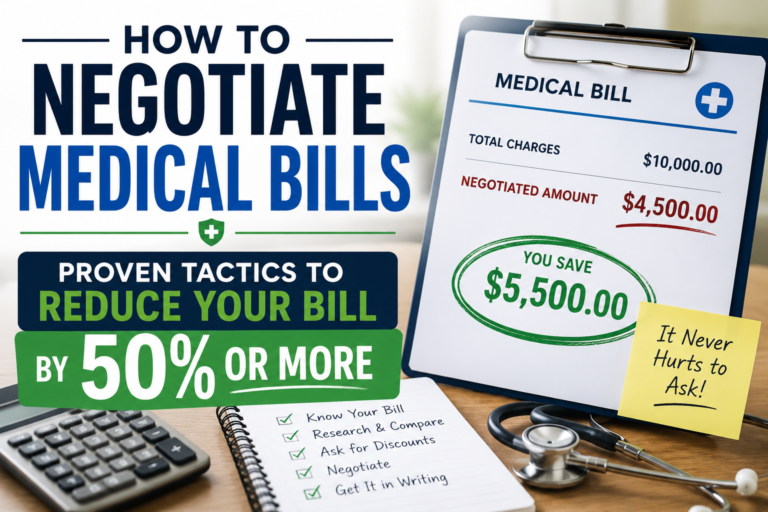

Option 3 — Negotiate a Lump Sum Settlement

If you have access to some funds — perhaps savings, a tax refund, help from family, or proceeds from selling something — you may be able to settle your hospital bill for significantly less than the full amount through a lump sum negotiation. Hospitals prefer a certain smaller payment over an uncertain larger one. This gives you negotiating leverage.

How Lump Sum Negotiation Works

Step 1: Determine the maximum lump sum you can offer — typically 40–60% of the total bill is a realistic starting target. Step 2: Call the billing department and say: “I have been reviewing my financial situation and I am not able to pay the full balance of [amount]. However, I do have access to [lower amount] that I could pay as a one-time lump sum settlement to resolve this account completely. Is this something your hospital would consider?” Step 3: If they agree, request written confirmation of the settlement terms before paying — specifically confirming that payment of [amount] resolves the account in full with no further balance owed. Step 4: Pay by check or money order — never pay a settlement in cash.

Typical Settlement Ranges

• Bills under $5,000 — hospitals often settle for 50–70% of balance • Bills $5,000–$20,000 — hospitals often settle for 40–60% of balance • Bills over $20,000 — hospitals have more flexibility — settlements of 30–50% are possible The older the debt, the more flexibility the hospital typically has. A bill that has been outstanding for 6 months or more is often settled for much less than face value.

Option 4 — Apply for Government Assistance Programs

There are several government programs that may help cover your hospital bill — many of which patients never think to apply for.

Medicaid Retroactive Eligibility

If your income qualifies you for Medicaid, you may be able to apply retroactively — meaning Medicaid could cover a hospital bill you already received. In most states, Medicaid can be applied retroactively for up to 3 months before your application date. This means if you had surgery 2 months ago and qualify for Medicaid today, Medicaid may cover that bill entirely. Contact your state Medicaid office or apply at healthcare.gov to find out if you qualify.

Children’s Health Insurance Program (CHIP)

If you have children under 19 who are uninsured or underinsured, they may qualify for CHIP — which could cover their medical bills including hospital stays. Apply at insurekidsnow.gov.

Hill-Burton Free Care Program

The Hill-Burton program is a little-known federal program that obligates certain hospitals and health facilities that received federal construction funding to provide free or reduced-cost care to people who cannot afford to pay. To find Hill-Burton obligated facilities near you, call the Hill-Burton hotline at 1-800-638-0742 or visit hrsa.gov/get-health-care/affordable/hill-burton.

State and Local Assistance Programs

Many states have their own programs beyond Medicaid for people who fall into the gap between Medicaid eligibility and private insurance affordability. Contact your state health department or call 211 (the social services helpline available in most US states) to find out what programs are available in your area.

Option 5 — Work With a Non-Profit Credit Counselling Agency

If your hospital bill is part of a larger pattern of unmanageable debt, a non-profit credit counselling agency can help you create a comprehensive debt management plan that addresses your hospital bill alongside other debts.

What Credit Counsellors Do

Non-profit credit counsellors: • Review your complete financial situation — income, expenses, all debts • Help you create a realistic budget • Negotiate with creditors on your behalf — including hospitals and medical debt collectors • Set up a Debt Management Plan (DMP) that consolidates your payments into one manageable monthly amount • Provide ongoing support and financial education

How to Find a Legitimate Non-Profit Credit Counsellor

Only work with agencies affiliated with the National Foundation for Credit Counseling (NFCC) at nfcc.org or the Financial Counseling Association of America (FCAA) at fcaa.org. These organisations are legitimate non-profits. Avoid for-profit debt settlement companies — they often charge high fees and can damage your credit further. Initial consultations with NFCC members are typically free. Full debt management plans usually cost $25 to $55 per month — a fraction of what for-profit companies charge.

How to Contact an NFCC Member Agency

Call the NFCC at 1-800-388-2227 — available Monday to Friday 8am to 8pm Eastern Time — to be connected with an NFCC member agency in your area.

Option 6 — Understand Your Legal Protections Against Collections

If your hospital bill has already gone to collections — or if you are worried it might — understanding your legal rights is essential.

The Fair Debt Collection Practices Act (FDCPA)

The Fair Debt Collection Practices Act gives you significant protections against debt collectors: • Collectors cannot call you before 8am or after 9pm • Collectors cannot call your workplace if you tell them your employer disapproves • Collectors cannot use abusive, threatening or profane language • Collectors cannot misrepresent the amount you owe • Collectors cannot threaten actions they cannot legally take • You have the right to request debt validation — the collector must prove the debt is valid and that they have the right to collect it

The Debt Validation Letter — Use This Within 30 Days

If you receive contact from a debt collector about a medical bill, send a debt validation letter within 30 days. This requires the collector to: • Verify the amount of the debt • Provide the name of the original creditor • Prove they are authorised to collect the debt While they are verifying, they must stop collection activity. This buys you time and sometimes reveals errors that invalidate the debt entirely. Debt validation letter: “[Your Name] [Your Address] [Date] [Collection Agency Name] [Collection Agency Address] Re: Account Number [X] — Request for Debt Validation Dear Sir or Madam, I am writing in response to your communication dated [date] regarding the above-referenced account. Pursuant to my rights under the Fair Debt Collection Practices Act (15 USC 1692g), I am requesting complete validation of this debt, including: 1. The name and address of the original creditor 2. The original amount of the debt 3. Documentation showing I am legally obligated to pay this debt 4. Proof that your company is licensed to collect debt in my state Until you provide this validation, I request that you cease all collection activity on this account. Sincerely, [Your Name]” Send by certified mail with return receipt requested.

Medical Debt and Your Credit Report — New 2023 Rules

Important changes to medical debt credit reporting took effect in 2023: • Medical debt under $500 no longer appears on credit reports from Equifax, Experian and TransUnion • Medical debt that has been paid is removed from credit reports immediately • There is now a one-year grace period before unpaid medical debt appears on credit reports — giving you more time to resolve bills before your credit is affected If you have medical debt on your credit report that violates these new rules, file a dispute directly with the credit bureau. You can do this for free at annualcreditreport.com.

Real Case Study — How One Family Managed a $47,000 Hospital Bill

When David and Maria R. from Florida faced a $47,000 hospital bill after David required emergency heart surgery, they were terrified. David was self-employed with no health insurance and their savings covered less than one month of living expenses. Here is what they did — and what happened: Week 1 — Called the billing department immediately Rather than ignoring the bill, David called within 3 days of receiving it. He explained his situation honestly and asked about all available options. The billing counsellor walked him through the charity care application process. Week 2 — Applied for charity care David and Maria submitted their charity care application with full documentation. Their combined income of $48,000 for a family of 4 put them at approximately 193% of the Federal Poverty Level — just under the 200% threshold for full bill forgiveness at their hospital. Result: $38,000 wiped out completely through charity care.Week 3 — Negotiated the remaining $9,000 The remaining $9,000 represented charges that fell outside the charity care program. David negotiated a lump sum settlement of $4,500 — 50% of the remaining balance — which the hospital accepted because David could pay immediately. Final outcome: • Original bill: $47,000 • Charity care forgiveness: $38,000 • Settlement of remaining balance: $4,500 • Total paid: $4,500 out of $47,000 • Total saved: $42,500 “I almost did not call because I was ashamed,” David said. “I thought hospitals only helped people in extreme poverty. I had no idea that a family earning $48,000 a year could qualify for almost complete forgiveness. The billing counsellor was incredibly kind about the whole thing.”

What NOT to Do When You Cannot Pay a Hospital Bill

Knowing what to avoid is just as important as knowing what to do. These are the most common and most damaging mistakes:

❌ Do NOT Pay with a High-Interest Credit Card

Using a credit card with 20–29% interest to pay a medical bill turns a manageable debt into a potentially unmanageable one. If you cannot afford the hospital bill, you almost certainly cannot afford to carry that balance on a credit card. Exception: If you have access to a 0% APR balance transfer card and are confident you can pay it off before the promotional period ends — this can be a useful strategy. But never use a standard high-interest credit card.

❌ Do NOT Use a Medical Credit Card Without Understanding the Terms

Cards like CareCredit offer promotional 0% financing — but if the balance is not paid in full before the promotional period ends, deferred interest kicks in retroactively from the original purchase date. This can add hundreds or thousands of dollars to your balance overnight.

❌ Do NOT Ignore Collection Letters

Ignoring collection letters does not stop the collection process — it accelerates it. Respond to every collection letter, even if just to request debt validation.

❌ Do NOT Pay Before Checking for Errors

Before paying any amount on any bill, request your itemised statement and check for errors. Studies show up to 80% of medical bills contain at least one error. Paying an incorrect bill is much harder to undo than catching the error first.

❌ Do NOT Use a For-Profit Debt Settlement Company

For-profit debt settlement companies charge fees of 15–25% of the total debt and often damage your credit further before settling. The same outcomes can be achieved for free or nearly free through non-profit credit counsellors and the strategies in this guide.

❌ Do NOT Assume Bankruptcy is Your Only Option

Bankruptcy should be a last resort — not a first response. The six options in this guide resolve the vast majority of hospital bill situations without the long-term credit consequences of bankruptcy. Exhaust every other option first.

Frequently Asked Questions

What happens if I simply cannot pay anything at all right now?

Call the hospital billing department immediately and explain your situation honestly. Ask to be connected with a financial counsellor. Explain that you have zero ability to pay at this time and ask about complete financial hardship programs. Most hospitals have provisions for patients in true financial crisis — including complete bill forgiveness in extreme cases. The key is to communicate proactively rather than going silent.

Can a hospital send me to collections while I am applying for charity care?

Many hospitals have policies preventing collections activity while a charity care application is pending. Ask the billing department about this policy when you submit your application and get the answer in writing. If the hospital does send your account to collections while your application is pending, file a complaint with your state Attorney General’s office.

Will applying for charity care affect my credit score?

No. Applying for a hospital’s financial assistance program is not reported to credit bureaus and has no impact on your credit score. Only unpaid bills sent to collections affect your credit — and charity care prevents that from happening.

What if I already paid the bill but I am now realising I could have qualified for charity care?

Contact the hospital billing department immediately. Explain that you recently paid a bill and are now aware you may have qualified for financial assistance. Request a retroactive charity care review. Some hospitals will process retroactive applications and issue refunds. This is not guaranteed but is absolutely worth pursuing.

Can I apply for charity care if I have health insurance?

Yes — in many cases. Charity care can cover costs that your insurance did not pay, including deductibles, copays and coinsurance. If you have insurance but still face a bill you cannot afford, apply for charity care for the remaining patient responsibility portion.

How long does the charity care application process take?

Most hospitals process charity care applications within 2 to 4 weeks. During this time, collection activity should be paused. Follow up in writing after 10 business days if you have not received confirmation that your application is being processed.

What if the hospital is for-profit and does not offer charity care?

For-profit hospitals are not required to offer charity care. However, many do offer financial assistance programs voluntarily. Always ask regardless of hospital type. Additionally, for-profit hospitals are often more willing to negotiate lump sum settlements than non-profit hospitals — so Option 3 (lump sum negotiation) may be particularly effective.

Your Complete Action Plan — Do This Today

Do not wait. The sooner you act, the more options you have available. Today: 1. Call the hospital billing department — tell them you cannot pay and ask about all available options 2. Ask for the charity care application — even if you think you might not qualify 3. Request your itemised bill — check for errors before committing to pay anything This week: 4. Complete your charity care application — gather all required documentation 5. Research Medicaid eligibility — apply retroactively if you qualify 6. Call 211 — find out what local and state assistance programs are available If charity care does not cover everything: 7. Negotiate a zero-interest payment plan — at an amount you can genuinely afford 8. Consider a lump sum settlement — if you have access to a portion of the funds 9. Contact an NFCC credit counsellor — if medical debt is part of a larger financial challenge If the bill is already in collections: 10. Send a debt validation letter immediately — within 30 days of first contact 11. Know your FDCPA rights — collectors must follow strict rules 12. Check your credit report — dispute any medical debt that violates the new 2023 rules You have more options than you realise. The hospital bill sitting on your kitchen table is not the final word — it is the opening position in a negotiation. Use every tool available to you. For more guidance on specific strategies, read our related guides: • How to Negotiate Medical Bills After Surgery — Save Up to 80% • How to Request an Itemised Medical Bill — Free Script Inside • How to Dispute a Medical Bill With Your Insurance CompanyMedical and Financial Disclaimer: The information on FightMedicalBill.com is for educational purposes only and does not constitute medical, legal or financial advice. Always consult a qualified professional for advice specific to your situation. Program eligibility, income thresholds and hospital policies vary and change regularly. Always verify current information directly with your hospital and relevant government agencies.