How to Read an Explanation of Benefits (EOB): A Complete Patient Guide for 2026

An Explanation of Benefits (EOB) is one of the most important documents in American healthcare — and one of the most confusing. It’s not a bill. It’s not a receipt. It’s a summary from your insurance company explaining what happened after a healthcare claim was submitted on your behalf. Understanding your EOB is essential for catching billing errors, understanding your actual financial responsibility, and knowing when to dispute a claim.

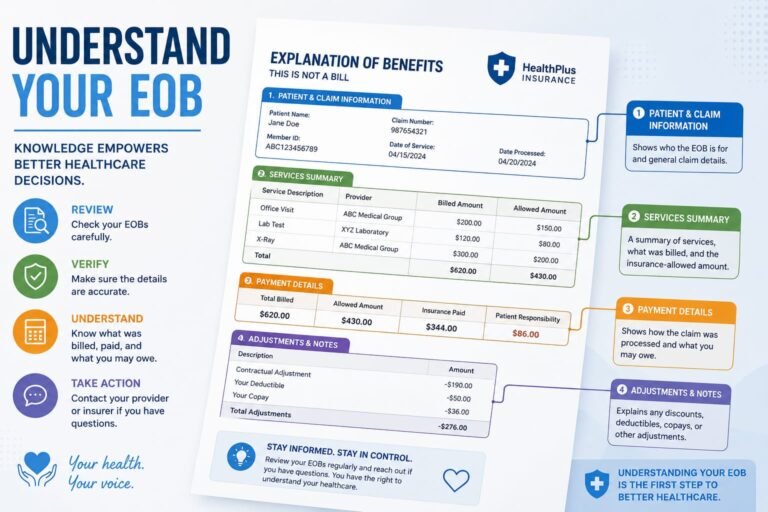

Key Sections of an Explanation of Benefits

Section 1: Patient and Claim Information

The top section of your EOB identifies: your name and member ID, the patient’s name (may differ if the service was for a dependent), the claim number (use this if you need to call your insurer), the date of service, and the name of the provider who submitted the claim. Verify all of this information is correct — errors in patient ID or provider information can cause claim misprocessing.

Section 2: What Was Billed

“Amount Billed” or “Charges Submitted”: This is what the provider charged — often the chargemaster rate, which can be far higher than what anyone actually pays. Do not be alarmed by this number. It’s the starting point of negotiation between your insurer and the provider, not what you owe.

Section 3: What Insurance Allowed

“Allowed Amount” or “Negotiated Rate”: This is what your insurance company has agreed is the maximum payable amount for this service — typically much lower than the billed amount for in-network providers. The difference between “Amount Billed” and “Allowed Amount” is called the “discount” or “contractual adjustment.” In-network providers have contractually agreed to accept the allowed amount as payment in full — they cannot bill you for the difference.

Section 4: What Insurance Paid

“Plan Paid” or “Insurance Paid”: What your insurance company actually paid the provider from the allowed amount. The calculation: Allowed Amount minus your deductible and coinsurance = Plan Paid.

Section 5: What You Owe

“Your Responsibility” or “Patient Responsibility”: What you legitimately owe after insurance has processed the claim. This is typically made up of:

- Deductible: Your remaining annual deductible amount applied to this claim

- Copay: Your fixed copay for this type of service

- Coinsurance: Your percentage share of the allowed amount (e.g., 20% after deductible is met)

- Non-covered amount: Services your plan doesn’t cover at all

Section 6: Reason Codes

Your EOB will include codes (letters, numbers, or short phrases) explaining how each line item was processed. Common reason codes to know:

- “Service not covered by this plan” — verify this is accurate; sometimes a covered service is denied due to incorrect coding

- “Deductible applies” — normal; your deductible is being applied

- “Prior authorization required” — claim denied because pre-approval wasn’t obtained; potential appeal opportunity

- “Duplicate claim” — claim denied as a duplicate; verify this isn’t a billing error creating a false duplicate

- “Not medically necessary” — significant appeal opportunity in many cases

How to Compare Your EOB to Your Medical Bill

When you receive both an EOB from your insurer and a bill from your provider, compare them side by side:

- Verify the services listed on the bill match the services on the EOB

- Verify the dates match

- The amount the provider bills you should match the “Patient Responsibility” on your EOB — not the original billed amount

- If the provider’s bill is higher than your EOB’s patient responsibility, contact your insurer before paying the difference

This comparison is where many billing errors are caught — providers sometimes bill patients for amounts beyond their legitimate patient responsibility under the insurance contract.

When to Appeal Based on Your EOB

Your EOB is your roadmap to insurance appeals. File an appeal when:

- A claim was denied for prior authorization you believe was properly obtained

- A service was denied as “not medically necessary” when your doctor ordered it as clinically required

- An in-network service was processed as out-of-network

- A covered service was denied under an incorrect reason code

- Your deductible or out-of-pocket accumulator appears incorrect

You have a legal right to appeal insurance denials. The EOB provides the claim number and denial reason — exactly what you need to initiate the appeal process.

Digital EOBs vs Paper EOBs

Most insurers now send EOBs digitally through your online member portal. Manage your EOB documentation by: saving all EOBs as PDFs organized by year and provider, cross-referencing digital EOBs with paper bills as they arrive, and using your insurer’s online portal to track cumulative deductible and out-of-pocket amounts applied to date.

Frequently Asked Questions

I received an EOB but no bill from the provider. What should I do?

Wait for the bill. The EOB shows you what’s coming but some providers mail bills separately. If you haven’t received a bill within 30 days and the EOB shows patient responsibility, call the provider’s billing department to confirm billing is in process and the address they have on file for you.

My EOB says a service was denied. Does that mean I owe the full amount?

Not necessarily. If a service was denied, you have the right to appeal the denial. Many denials — particularly for “medical necessity” reasons — are overturned on appeal. Appeal before paying anything based on a denial. See our guide on medical bill errors for dispute strategies.

What if my EOB shows my out-of-pocket maximum was already met but I’m still being charged?

This is an error. Once your annual out-of-pocket maximum is met, your plan pays 100% of covered services for the rest of the plan year. Contact your insurer immediately with your EOB showing the out-of-pocket accumulator.

Conclusion

Your EOB is one of your most powerful tools for managing healthcare costs — but only if you read it. Taking 10 minutes to review each EOB before paying any medical bill can prevent overpayments, identify billing errors, and give you the information needed to dispute improper denials. In a healthcare billing system with an 80% error rate, patient vigilance is the most reliable quality control mechanism available. Use your EOB as the authoritative reference it’s designed to be, and always verify that what the provider is charging you matches what your insurance says you owe.

Download Our EOB Comparison Worksheet

Side-by-side template for matching your EOB against your medical bill.