Hospital Financial Assistance Programs 2026: How to Get Your Medical Bills Reduced or Forgiven

Here’s something most hospitals will never tell you upfront: they are legally required to help you pay your bill if you can’t afford it. Not as a favor. Not as charity in the traditional sense. As a legal obligation tied to their nonprofit tax status.

Yet fewer than 1 in 10 patients who qualify for hospital financial assistance ever apply for it. Most people either don’t know these programs exist, assume they won’t qualify, or give up when the process seems complicated. This guide changes that.

What Are Hospital Financial Assistance Programs?

Hospital Financial Assistance Programs — also called charity care programs, sliding scale programs, or FAPs — are formal programs that reduce or completely eliminate medical bills for patients who meet income and eligibility requirements.

These aren’t handouts. They are structured programs with specific rules, income thresholds, and application processes. The key is knowing they exist and applying before your bill goes to collections.

Who Offers These Programs?

All nonprofit hospitals in the United States — which represent approximately 58% of all hospitals — are legally required to offer financial assistance programs under the Affordable Care Act. Many for-profit hospitals also offer assistance programs voluntarily, though the terms vary more widely.

Income Limits: Do You Qualify?

This is where most people are surprised. Financial assistance income limits are often far higher than people expect. The thresholds vary by hospital, but here are typical examples:

| Income Level (% of Federal Poverty Level) | Typical Assistance Level |

|---|---|

| Under 100% FPL (~$15,060 for individual) | Full bill forgiveness (100%) |

| 100–200% FPL (~$15,060–$30,120) | 75–100% reduction |

| 200–300% FPL (~$30,120–$45,180) | 50–75% reduction |

| 300–400% FPL (~$45,180–$60,240) | 25–50% reduction |

| Above 400% FPL | Sliding scale, varies by hospital |

For a family of four in 2026, the federal poverty level is approximately $31,200. That means a family of four earning up to $93,600 per year (300% FPL) may qualify for significant financial assistance at many hospitals.

Step-by-Step: How to Apply for Hospital Financial Assistance

Step 1: Request the Financial Assistance Application

Call the hospital billing department and say: “I would like to apply for your Financial Assistance Program.” They are required to provide you with an application. Under ACA rules, hospitals must also make FAP applications available on their website and in their billing offices.

Step 2: Gather Your Documentation

Most applications require:

- Proof of income (pay stubs, tax returns, or bank statements from the last 3 months)

- Proof of household size (birth certificates, tax returns listing dependents)

- Photo ID

- Insurance information (even if you have insurance, you may qualify for assistance on your remaining balance)

- Social Security numbers for household members (some hospitals require this)

Step 3: Complete and Submit the Application

Fill out the application completely and accurately. Incomplete applications are the most common reason for delays or denials. Submit via certified mail or in person, keeping a copy for your records. Note the date of submission.

Step 4: Follow Up

Most hospitals process applications within 2 to 4 weeks. Follow up after 10 business days if you haven’t heard back. Ask for the name of the financial counselor handling your application.

Step 5: If Denied, Appeal

If your application is denied, you have the right to appeal. Common reasons for denial include incomplete documentation or income calculations that can be reinterpreted. Ask for the specific reason for denial and provide additional documentation that addresses it.

What If You Already Have Insurance?

Having insurance doesn’t disqualify you from financial assistance. Many hospitals will apply charity care to your remaining patient responsibility after insurance pays — including deductibles, copays, and coinsurance. This is particularly valuable for patients with high-deductible health plans facing large out-of-pocket costs.

Other Programs to Know About

Medicaid Retroactive Enrollment

If you didn’t have Medicaid at the time of your hospital visit but you’re income-eligible, you may be able to enroll retroactively and have Medicaid cover past bills. Many states allow retroactive Medicaid coverage for up to 3 months before the application date.

Hill-Burton Hospitals

Some older hospitals received federal funding under the Hill-Burton Act and are obligated to provide free or reduced-cost care to eligible patients. You can search for Hill-Burton facilities through the Health Resources and Services Administration (HRSA) website.

Disease-Specific Assistance Programs

Many pharmaceutical companies, disease foundations, and nonprofit organizations offer financial assistance for specific conditions — cancer, diabetes, heart disease, mental health, and more. These programs can cover treatments, medications, and follow-up care beyond what standard hospital financial assistance covers.

State and County Indigent Care Programs

Many states and counties have their own indigent care programs that operate independently of hospital charity care. These vary widely by location — contact your county health department to learn what’s available in your area.

What Happens to Your Bill While You Apply?

This is a critical question. Under ACA rules, nonprofit hospitals must suspend billing and collection activities while a financial assistance application is pending. They cannot send your bill to collections, report it to credit bureaus, or take legal action while your application is being reviewed.

This protection is significant. Once you submit your application, you have formal protection against collection while the hospital reviews it. Make sure to submit something in writing even if your application is not yet complete — the protection begins when you notify them you’re applying, not when the application is finalized.

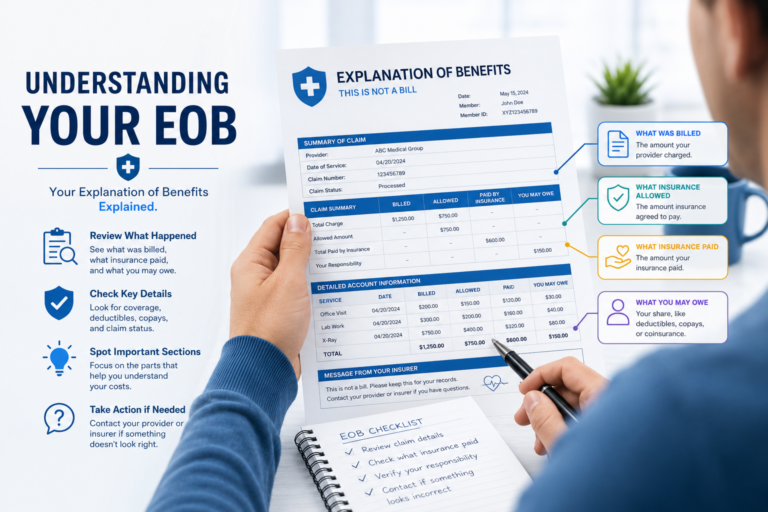

For a complete understanding of your rights when medical debt does reach collections, read our guide on medical debt and your credit score.

Real Examples: What Financial Assistance Can Look Like

Example 1: A single mother of two earning $28,000 per year receives a $12,000 emergency room bill. At 180% of the federal poverty level for a family of three, she qualifies for 80% assistance at her nonprofit hospital. Her final bill: $2,400.

Example 2: A self-employed contractor earning $45,000 per year faces a $30,000 surgery bill. At 250% FPL for a single person, he qualifies for 50% assistance. His final bill: $15,000 — eligible for an interest-free payment plan of $208/month.

Example 3: A retired couple earning $22,000 per year faces $8,000 in combined medical bills. At under 150% FPL, they qualify for full forgiveness. Their final bill: $0.

Tips for a Successful Application

- Apply as early as possible — don’t wait until bills go to collections

- Apply even if you think you might not qualify — you may be surprised

- If you have multiple bills from the same hospital, one application typically covers all of them

- Keep copies of everything you submit and all correspondence

- Ask specifically about the income threshold for full forgiveness — many people qualify without realizing it

- If language is a barrier, hospitals are required to provide interpreter services and translated materials

Remember: before applying for assistance, make sure your bill is accurate. Check out our comprehensive guide to reading your hospital bill to identify and dispute errors first — then apply for financial assistance on the corrected amount.

Frequently Asked Questions

Will applying for financial assistance hurt my credit?

No. Applying for financial assistance has no impact on your credit score. In fact, it can help your credit by preventing an unpaid bill from going to collections.

Can I apply for financial assistance after my bill has gone to collections?

In many cases, yes. Contact the hospital directly — not the collection agency — and ask to apply for financial assistance. Many hospitals will recall a bill from collections if you qualify for their program.

What if the hospital says they don’t have a financial assistance program?

If the hospital is a nonprofit, they are legally required to have one. Ask to speak with a patient financial counselor or patient advocate. If the hospital is for-profit, ask about their charity care or reduced-cost care options — many still offer assistance even without a formal program.

How often can I apply?

Financial assistance is typically applied per billing episode or per year. If your financial situation continues, you may need to reapply annually or for each new set of bills.

Final Thoughts

Hospital financial assistance programs are one of the most underutilized resources available to American patients. The money is there. The programs exist. The legal requirements are in place. The only thing standing between millions of struggling patients and significant relief is knowing to ask.

Don’t let embarrassment, intimidation, or assumption stop you from applying. This isn’t charity in the traditional sense — it’s a legal program that exists because of your tax dollars and the nonprofit status these hospitals enjoy. You have every right to apply, and doing so could eliminate thousands of dollars in medical debt.

Take the first step today: call your hospital’s billing department and ask for a financial assistance application.

You May Qualify for Free or Reduced Medical Care

Don’t pay your hospital bill until you’ve checked what assistance you qualify for.